Are you a private sector employer? Have you considered the benefits of Group Personal Pension Schemes?

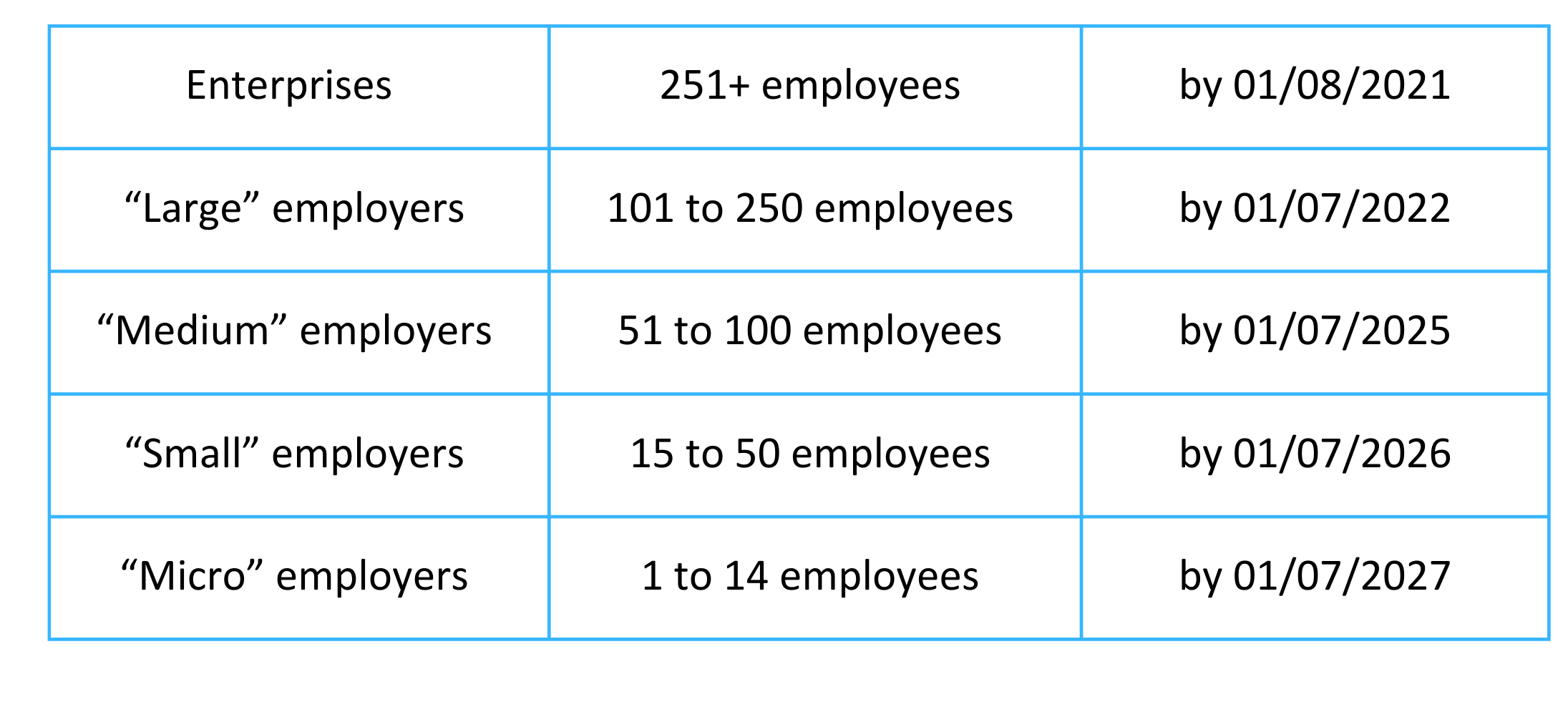

Following the introduction of the Private Sector Pensions Act 2019 (“the Act”) all employers within Gibraltar’s private sector must provide their employees with access to a pension scheme.

You have two options by which you can discharge your legal obligations, Group Personal Pension Schemes and Occupational Pension Schemes, and we find that many employers look for guidance as to the benefits and drawbacks between them.

As the decision as to which type of scheme best suits each employer may vary, we would be delighted to assist you and your company in making this decision and set out some initial commentary below.

Group Personal Pension Scheme ever more popular for both employers, and

employees

Group Personal Pension Schemes make up a large, and ever-increasing proportion of the

UK workplace pensions market.

We see Gibraltar following a similar trend.

Why? Due to the added flexibility these offer and the higher levels of responsibility and

administration burdens which Occupational Pension Schemes place on the employer.

With Occupational Pension Schemes, the employer is responsible for the scheme itself,

its members, its assets/investments, providing and reviewing investment options allowed

to its members, preparing annual reports, audits, and trustee liability insurance for

example, as well as the amount of legislation and trust law to understand and adhere to.

Further, if the employee/member leaves, they leave their portion of the scheme behind,

and the employer is still responsible for it until retirement.

A Group Personal Pension Scheme by comparison is trust-based (i.e. managed by

trustees who have a fiduciary duty to act in the best interests of the scheme). With these

schemes the employer needs to appoint a pension provider/trustee to run the scheme

and engage an independent wealth management firm to manage the investments (albeit

following employee choices based on risk appetite).

In this case the employer’s only requirement is to ensure contributions are paid on time.

All other responsibilities they would have for an Occupational Pension Scheme become

those of the pension provider/trustee. The employer has no responsibility for the

investments, the trustee relationship is between the pension provider/trustee and the

employee/member and if employees/members leave the company, their pension

effectively goes with them and is their responsibility and not that of the employer.

Independent Wealth Management

Given the impact pension schemes have on a person’s future financial stability, our clients

truly appreciate the ability to choose independent financial advisors.

They offer a broader range of expertise and unbiased perspectives, enhanced decision-

making through diverse insights and experience, and thereby reducing potential conflicts

of interests and ensuring adherence to the highest standards of fiduciary responsibility.

The choice of independent financial advisors can then be based on performance and

access to specialised knowledge and resources whilst retaining clarity of their respective

roles and responsibilities.

Where assistance is required in making this choice as to independent financial advisor, we

have access to a number of financial advisors who are qualified to provide independent,

individual and regulated financial/investment advice, as well as investment management

and employee benefit services to pension members.

We work with a multitude of financial advisors which our clients are free to choose from

and we are also open to working with others you may choose who are equally

credentialed.

The choice is yours.

Should you wish to obtain further information or discuss how the Act applies to you and

your business please do contact our experienced team and have them guide you through

your options and obligations.

wayne.fortunato@linegroup.gi

yvonne.victor@linegroup.gi

peter.donovan@linegroup.gi

Subscribe to more insights from our experts at Hassans Subscribe now!

/Passle/5e2ef0738313d50b64779f79/MediaLibrary/Images/2026-07-31-09-22-44-384-6a6c6964700fbea3a806afa4.png)

Gibraltar Opens the Door to Tokenised Fund Shares: What It Means and Who Can Use It

DLT now sits inside Gibraltar's statutory framework for investment funds, a step most jurisdictions have discussed without legislating...

/Passle/5e2ef0738313d50b64779f79/MediaLibrary/Images/2026-07-30-07-33-10-238-6a6afe36464b8cfe78d68c10.png)

/Passle/5e2ef0738313d50b64779f79/MediaLibrary/Images/2026-07-24-08-35-46-453-6a6323e2e30065ccfb6ba926.png)